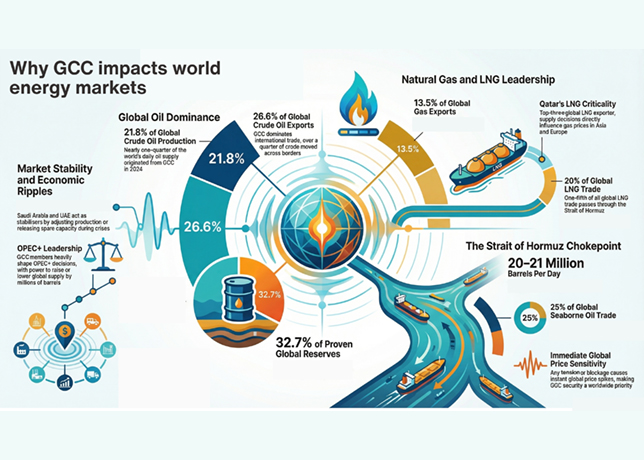

Disruption in Gulf shipping lanes imperils oil supply and global growth

The Strait of Hormuz, a 33-39 km-wide waterway at its tightest point, through which roughly 20 million barrels per day (bpd) of crude transit (about 20 per cent of global oil consumption), has ceased normal maritime throughput as geopolitical conflict escalates.

With tanker traffic curtailed to a trickle and insurers repricing risk aggressively, the corridor’s closure has removed an estimated 9 million bpd from global supply, driving Brent crude to surge by more than 50 per cent in March and prompting options markets to signal a non trivial probability of prices near $150 per barrel or higher.

War risk insurance premiums for vessels in the region have jumped sharply, with market reports noting increases to 5-10 per cent of a ship’s insured value, up from fractions of a per cent in peacetime.

This escalation has pushed freight costs on key Middle East routes to figures equivalent to more than $400,000 per day, effectively pricing many operators out of transit and forcing cargoes to reroute around the Cape of Good Hope, adding weeks to voyages and materially increasing delivered cost.

Analysts have projected that a sustained closure lasting two quarters could lift oil to average $115 per barrel and depress global GDP growth by around 0.3 percentage points in 2026, with impacts growing if the disruption persists.

Beyond oil, the bottleneck threatens LNG and petrochemical flows, with Asia, the destination for roughly 80 per cent of Gulf exports, facing acute supply and price pressures.

The combined effect on energy costs, inflation and global trade underscores that a closed Hormuz is not a regional problem but a structural shock to the world economy.

By Abdulaziz Khattak