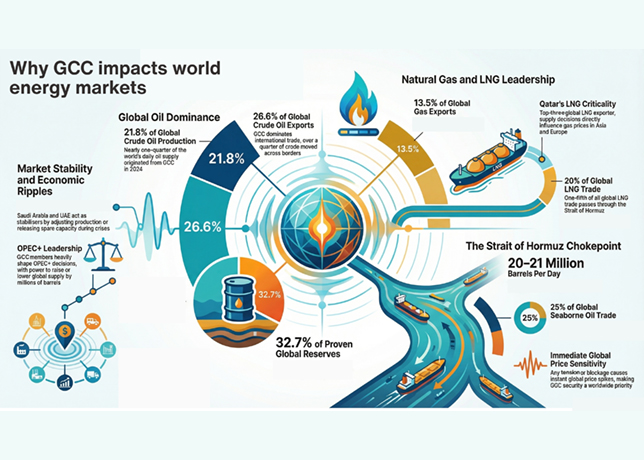

GCC states, which include Saudi Arabia, the UAE, Kuwait, Qatar, Bahrain and Oman, remain pivotal to the global energy system, producing 21.8 per cent of global crude oil and 26.6 per cent of exports in 2024

Output averaged 16.1 million barrels per day (bpd) and exports 11.5 million bpd, down 5.4 per cent and 7.2 per cent from 2023.

The region controls 511.9 billion barrels of oil reserves, equivalent to 32.7 per cent of the global total, and 44.3 trillion cu m of natural gas, or 21.2 per cent worldwide.

GCC natural gas output contributed 10 per cent of worldwide production, with exports at 13.5 per cent.

Supply flows are heavily concentrated toward Asia, particularly China, India, Japan and South Korea, yet market effects are global due to oil’s benchmark pricing.

OPEC+ coordination, where Saudi Arabia and the UAE exert decisive influence, allows rapid adjustment of production, supporting prices during downturns or easing tightness.

Qatar’s LNG infrastructure anchors long-term contracts while engaging in spot markets affecting European and Asian pricing.

Even a one million bpd production shift can materially affect global balances.

GCC reserves and export infrastructure, combined with coordinated policy measures, secure the region’s structural influence on energy markets.

Hydrocarbon flows from the Gulf are integrated into worldwide supply chains, underpinning industrial activity, transportation, electricity generation, and manufacturing costs across continents.