The GCC supplies more than a fifth of global crude oil production and controls a third of proven reserves, positioning the bloc as a pivotal force in international energy supply and pricing dynamics

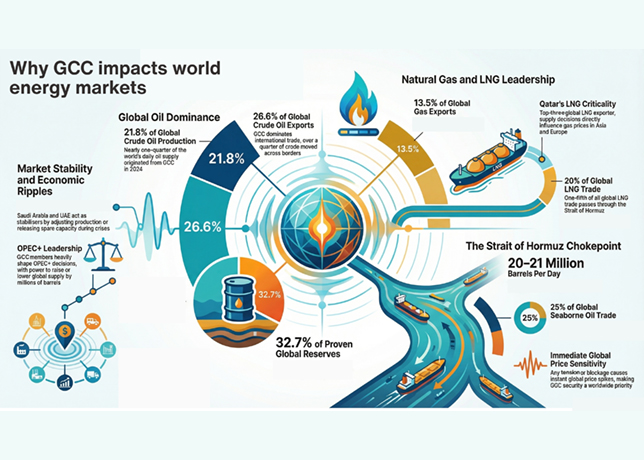

The Gulf Cooperation Council (GCC) member states, including Saudi Arabia, the UAE, Kuwait, Qatar, Bahrain and Oman, delivered 21.8 per cent of global crude oil production and 26.6 per cent of global crude oil exports in 2024, according to the GCC Statistical Center.

Production averaged 16.1 million barrels per day (bpd) after a 5.4 per cent decline from the previous year, while exports stood at 11.5 million bpd following a 7.2 per cent reduction.

The region held 511.9 billion barrels of crude oil reserves at the end of 2024, equivalent to 32.7 per cent of the world’s proven total, alongside 44.3 trillion cu m of natural gas reserves representing 21.2 per cent of the global figure.

In natural gas, the GCC contributed 10 per cent of worldwide marketed production and 13.5 per cent of global gas exports.

These volumes translate into structural influence over energy markets because oil remains a globally priced commodity.

Adjustments in GCC output, particularly through the OPEC+ framework where Saudi Arabia and the UAE hold significant sway, affect benchmark prices that determine costs for transportation, manufacturing, electricity generation and consumer goods across continents.

Even nations with minimal direct imports from the Gulf experience the consequences through integrated trading systems and price benchmarks.

STRATEGIC PRODUCTION & EXPORT CONCENTRATION

GCC hydrocarbon output flows predominantly toward high-demand markets in Asia, yet the scale of supply ensures worldwide repercussions.

Saudi Arabia, the UAE, Kuwait and others channel the majority of their crude toward China, India, Japan and South Korea, while Qatar directs substantial liquefied natural gas cargoes to the same destinations.

The concentration amplifies the region’s leverage, as any sustained change in availability or pricing reverberates through supply chains that underpin global economic activity.

Decision drivers for GCC energy policy centre on balancing revenue needs, long-term reserve management and market stability.

Production quotas within OPEC+ serve as the primary mechanism for coordinating supply responses to demand fluctuations or external shocks.

Spare capacity maintained by key producers such as Saudi Arabia enables rapid adjustments that can either support prices during downturns or ease tightness when required.

Natural gas strategy, led by Qatar’s LNG infrastructure, focuses on long-term contracts that secure steady offtake while allowing participation in spot markets that link European and Asian pricing.

The narrow Strait of Hormuz constitutes the most critical logistical pivot. In 2024, approximately 20 million bpd of crude oil and petroleum products transited the waterway, accounting for about 20 per cent of global petroleum liquids consumption and more than one-quarter of global seaborne oil trade.

Roughly 20 per cent of worldwide LNG trade also passed through the strait, primarily cargoes originating from Qatar.

These flows represent a genuine chokepoint, and disruption at this location immediately constrains available volumes on international markets and elevates prices irrespective of direct import dependence in any single consuming region.

IMPLICATIONS FOR MARKET STABILITY & ENERGY SECURITY

Forward-looking implications stem directly from the scale of GCC reserves and export infrastructure.

With 32.7 per cent of global oil reserves, the region retains capacity to influence supply trajectories for decades, provided investment in upstream projects continues.

Natural gas reserves at 21.2 per cent of the world total support Qatar’s position as a leading LNG supplier, with cargoes that integrate previously regional gas markets into a more connected global system.

Renewable energy capacity in the GCC reached 14.2 gigawatts in 2024, yet this remains a small fraction of global totals and does not yet alter the dominance of hydrocarbons in export profiles.

Market participants monitor GCC decisions because production changes of even one million bpd can shift global balances materially.

Opec+ coordination, driven by Gulf members, has demonstrated the ability to withhold or release volumes in response to inventory levels and demand signals.

The 2024 decline in GCC crude output and exports occurred amid broader efforts to manage market conditions, illustrating how internal policy choices translate into external price effects.

Global energy security calculations incorporate the Hormuz route because alternative pathways cannot quickly compensate for lost volumes.

Asian importers absorb the largest shares of GCC crude and LNG, but price formation occurs on a worldwide basis. European buyers, even after diversifying gas sources, encounter higher costs when LNG tightness emerges from reduced Qatari shipments. North American and other consumers face indirect exposure through refined product markets and feedstock prices for petrochemical industries.

The interplay between production volumes, reserve longevity and chokepoint vulnerability sustains the GCC’s role as a central reference point for energy analysts and policymakers.

Data from 2024 confirm that the region’s contributions, which include 21.8 per cent of oil production, 26.6 per cent of oil exports, 10 per cent of gas production and 13.5 per cent of gas exports, embed its influence within the architecture of global supply.

Reserve holdings of 511.9 billion barrels of oil and 44.3 trillion cu m of gas further anchor this position, ensuring that developments in the Gulf continue to register across international energy balances.

By Abdulaziz Khattak