Heat exchangers industry is a highly mature market

Heat exchangers industry is a highly mature market

While increasing industrial activities in developing countries is a crucial driver boosting the global heat exchangers market, the increasing competition due to entry of new vendors could pose a challenge to the growth of this market

The global market for heat exchangers is projected to reach $24.3 billion by 2020, driven by recent innovations in energy efficient heat exchangers; the soft recovery in global manufacturing purchasing managers index (PMI) and the ensuing improvement in investments in plant capacity expansion and upgrades.

According to a transparencymarketresearch.com report, the global heat exchanger market revenue was valued at $11.86 billion in 2013 and is expected to reach $24.3 billion by 2020, growing at a compound annual growth rate (CAGR) of 6.02 per cent from 2013 through 2020.

One of the key factors contributing to this market growth is the increasing industrial activities in developing countries. The market has also been witnessing the increasing adoption of energy-saving equipment. However, the increasing competition due to entry of new vendors could pose a challenge to the growth of this market.

Key vendors dominating this space include Alfa Laval, GEA Group, and Xylem. Other vendors are API Heat Transfer, Balcke-Durr, Chicago Bridge & Iron Company, Hisaka Works, Modine Manufacturing Company, SPX Corporation, Air Products and Chemicals, Tranter, Barriquand Technologies Thermiques, Hamon Group, Harsco Industrial Air-X-Changers, Sondex, SmartHeat and Vahterus, among others.

Heat exchangers are widely used in industrial oil coolers, boiler coolers, chilled water systems, transmission and engine coolers, condensers, and evaporators in refrigeration systems. These applications incur excessive loss of energy during the transfer of heat. Many industries are adopting high-end energy-saving heat exchangers to mitigate the erosion of their revenue, which is largely due to the rise in the cost of energy. Heat exchanger manufacturing companies such as Alfa Laval and GEA Group are investing heavily in research and development (R&D) to develop energy-efficient heat exchangers. This trend is expected to contribute toward the growth of the global heat exchanger market during the forecast period.

Increasing industrial activities in developing countries is a crucial driver boosting the market. Process and discrete industries in these countries have been expanding their manufacturing operations worldwide, which in turn is boosting the global heat exchanger market.

Further, one of the main challenges in this market is the increasing competition brought in by the entry of new vendors. The new vendors offer their products at a cheaper price, which makes the pricing more competitive and erodes the profit margins of the major players.

MARKET INSIGHTS

Heat exchangers are essential heat transfer devices used in all modern industrial, engineering, and commercial applications ranging from automotive, aerospace, commercial building heating ventilation air conditioning (HVAC) to heating, cooling, and heat recovery applications in industrial plants, manufacturing facilities and power plants. A core component of all thermal systems, heat exchangers are vital and indispensable to energy conversion and utilisation.

Demand in the market is driven by rapid industrialisation in developing countries and increasing investments in manufacturing plant infrastructures. The highly mature global heat exchangers market is set to thrive on replacement demand coming from frequent upgrades and incremental technology improvements. The market will continue to be driven by technology innovation and development. Also poised to drive future gains are innovations that help lower total ownership costs, increase durability and efficiency of heat exchangers, and reduce vibration induced premature failures.

Of special interest is the emergence of micro channel heat exchangers, a new generation heat exchangers flaunting potential applications in a wide range of diverse industries ranging from automotive, residential HVAC, to process industries.

Maximising thermal efficiency is the primary reason behind an increased demand for heat exchangers. A heat exchanger is a piece of equipment designed and built for efficient heat transfer from one medium to another. The media may be separated by a solid wall to prevent mixing or they may be in direct contact with the materials being processed, which could harm the end product.

These are widely used for space heating, refrigeration, air conditioning, in power plants, chemical plants, petrochemical plants, petroleum refineries, natural gas processing plants, and sewage treatment plants. The common example of a heat exchanger is found in an internal combustion engine, in which a circulating fluid known as engine coolant flows through radiator coils and air flows past the coils, cooling the coolant and releasing the heat generated by the engine, into open air.

Rapid growth in power consumption from the industrial sector is further contributing to the rapid pace of growth for the heat exchanger market. Condensers are a crucial element of any power station. They are the interface between the water/steam cycle and the heat sink. Condenser performances have a direct impact on the power station’s output and the availability of electric power. Condensers need to meet sustained high-performance requirements, since any rise in pressure at the turbine exhaust may cause substantial power loss.

This inevitable category of heat exchanger is implemented in most power generation plants across the globe. Thus, demand for heat exchangers will necessarily grow as new power stations are established.

Moreover, the fabrication costs of heat exchangers have declined as technology has progressed. Modern plate heat exchangers use pressed plates, which are less expensive than the welded plates used on earlier models. Pressed plates are also more resistant to corrosion and chemical reactions that could weaken the heat exchanger and hence require more frequent replacement. Many heat exchanges have even been modified with particular attention given to the ease of cleaning the equipment. For example, with plate heat exchangers, one can easily remove and replace plates individually rather than needing to take the whole system apart.

Many modern heat exchangers are very adaptable, which makes them suited for a wide variety of tasks. Presently, heat exchangers are manufactured with a compact and efficient design, which makes them useful in mobile applications. Though early heat exchangers were often as large as a refrigerator, heat exchangers, today are as small portable heaters. Heat exchangers are also quite flexible, because the fluid used to mediate the thermal exchange can be modified as per design specifications. This is an integral factor that has a long-term impact on the operations’ cost of the process plant as well as the equipment.

|

Modern heat exchangers are very adaptable |

PLATE EXCHANGERS GROWING 9.3PC

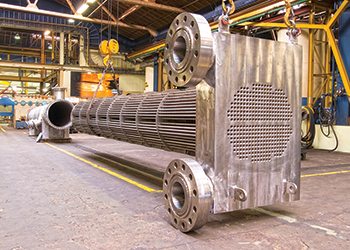

Plate and frame heat exchangers are commonly used heat exchangers in process industries and other applications. These consist of a series of slender corrugated formed metal plates. Every pair of plate’s form a passage in which the fluid flows. They are then stacked collectively to form a sandwich type construction in which the other fluid flows in the spaces created between successive pairs of plates.

On the basis of type plate and frame heat exchangers are classified as gasketed, welded, and brazed. On the basis of applications, the market for plate and frame heat exchangers can be broadly segmented into chemicals, petrochemical and oil and gas, heating ventilation air conditioning and refrigeration (HVACR), food and beverage, pulp and paper, power generation.

Currently, the demand for plate and frame heat exchangers is increasing in the end user industries. The key drivers for increasing demand of plate and frame heat exchangers are stringent environmental regulations, and increased investments in the food and beverage, chemical, oil and gas, and HVACR industries. Technological developments and innovations, agreements, partnerships and collaborations are identified as key strategies to expand the plate and frame heat exchangers market.

FUTURE GROWTH

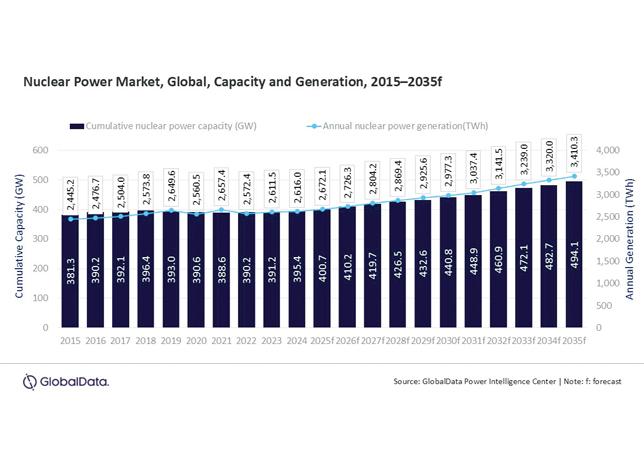

In the coming years, Greenfield projects in the energy industry, especially in the nuclear power sector, will support demand. Demand for heat exchangers in the nuclear power sector is poised to witness the highest growth given the encouraging number of new plants in the pipeline. Future growth will also be largely supported by the growing emphasis on energy savings and the ensuing need to reduce heat energy costs. The growing global focus on energy efficiency against a backdrop of depleting fossil fuel resources, rising focus on green energy and emphasis on curbing environmental pollution and climate, is poised to benefit the market for energy efficient heat exchangers.

Environmental concerns are likely to expedite the adoption of energy efficient products like compact heat exchangers and closed circuit cooling towers. The chemical industry also offers steady growth opportunities for heat exchangers in chemical processing and production applications. Stringent wastewater treatment laws, against a backdrop of rising levels of water pollution and contamination, are providing fertile opportunities for the growth of heat exchangers in wastewater treatment plants.

EUROPE: BIGGEST MARKET

Europe has always been a strong market for heat exchangers and globally this market has been a leader for heat exchangers with respect to demand as well as production capacity. The region has the presence of most of the global leaders in heat exchanger manufacturing. Heat exchanger consumption in the region is estimated to grow at a CAGR of around 4.81 per cent from 2014 to 2019 according to a marketsandmarkets.com report. This region has a relatively slow growth rate as a result of its dominant market size and slow economic activity as compared to the other regions. The demand in this region is boosted mainly due to the increased replacement demand for the heat exchangers.

Currently Europe acquires more than 30 per cent of the total global market. The region has huge installed plant capacities of heat exchanger and is an export based heat exchanger market. Also large number of emerging manufacturers from Eastern Europe is expected to reduce import dependence of various countries which is further expected to drive the heat exchanger market in future.

APAC: FASTEST GROWING MARKET

Asia-Pacific being the fastest growing heat exchangers market globally is estimated to grow at a CAGR of 10.70 per cent for the next five years. Asia-Pacific is witnessing high industrial growth rate which hints at an ever-increasing demand of heat exchangers for its diverse applications. Growth in the region is led by broad economic factors such as rising income levels, rapid urbanisation, strong industrialisation, expanding manufacturing/industrial base, growing middle class population, favourable demographics, government focus on infrastructure development, and energy self-sufficiency, among others.

China is expected to witness strong growth in its heat exchangers market due to growing demand from chemical petrochemical and oil amp; gas industry. HVAC industry is also growing at a healthier pace in this region. China dominates the heat exchangers market in Asia-Pacific region being a major consumer and the fastest growing country in terms of heat exchangers demand. Currently a high share of heat exchanger is being consumed by the chemical industry and the demand of heat exchangers through chemical industry is projected to grow in the next five years at a CAGR of 14.32 per cent from 2014 to 2019. After China countries such as India Japan and other Asian countries are showing increasing growth in demand for heat exchangers. Moreover increasing number of heat exchangers manufacturers from Asian countries are putting vigorous efforts for developing a strong base of heat exchanger market with a target of reducing heat exchanger imports.

CHINA DOMINATES AUTOMOTIVE MARKET

As key automotive components, automotive heat exchangers include radiators, evaporators, condensers, air coolers, oil coolers, exhaust gas recirculation (EGR) coolers and the like.

In 2014, there were around 500 heat exchanger manufacturers in China, including 10 large-sized enterprises and over 30 medium-sized ones. In the field of automotive heat exchangers, the world’s renowned companies like Delphi, Denso, Modine, Valeo and Visteon have set up factories in China by sole proprietorship, joint ventures or holding companies. In addition, local Chinese brands are emerging, such as Zhejiang Yinlun, Weifang HengAn, GuizhouYonghong, Yangzhou Tank, NanchongKangda, Nanning Baling, etc.

Driven by automobile output and replacement demand, China’s market demand for automotive heat exchangers will keep a growth rate of about 7 per cent; wherein, pressurised intercoolers and EGR coolers will continue to maintain high growth, with the growth rate of beyond 15 per cent.

Intercoolers are mainly installed in heavy-duty trucks, large buses, some medium and light-duty buses. Major Chinese intercooler manufacturers consist mainly of Shanghai BHER, Zhejiang Yinlun Machinery, Jiangsu Jiahe Thermal System Radiator, and Ningbo Lurun Cooler.

EGR coolers are important parts of EGR system. In China, EGR system is mainly applied to light trucks and European heavy trucks. Up to now, Chinese EGR system and parts enterprises embrace Wuxi Longsheng, YibinTianrui Da, Zhejiang Jiulong, Zhejiang Yinlun Machinery, KunshanPierburg, Ningbo BorgWarner and so forth. Zhejiang Yinlun Machinery is primarily engaged in EGR coolers at present. With the implementation of the national emission standards IV, EGR + DOC + POC will become the mainstream under the premise of light commercial vehicles using common rail technology; by then, EGR system and parts companies will see good prospects for development.