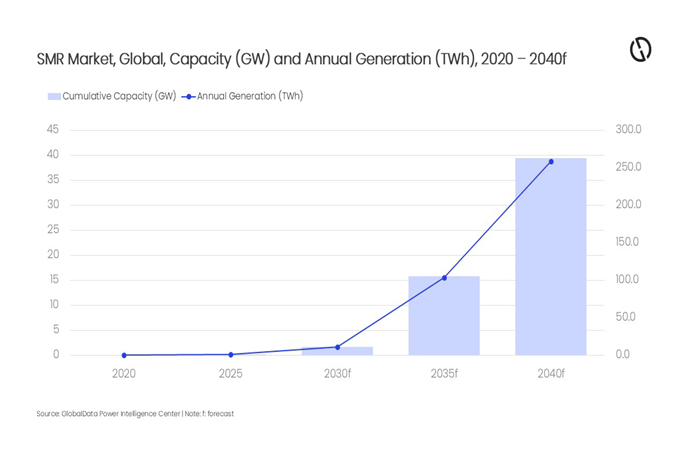

Small modular reactors (SMRs) are emerging as a key technology in the global shift to low-carbon, secure and flexible energy systems, with capacity forecast to rise roughly sixfold between 2025 and 2030, according to GlobalData.

In its report SMR Power Market, Update 2026 – Market

Size, Segmentation, Major Trends, and Key Country Analysis to 2035,

GlobalData says deployment strategies vary by region.

China is advancing multiple designs including light-water

SMRs, high-temperature gas reactors and molten-salt prototypes, while South

Korea is focusing on integral pressurised water reactors and

desalination-capable systems.

However, the sector remains largely early-stage, with more

than 90 per cent of proposed capacity still in announcement or permitting

phases.

The report warns that commercial success will depend on

whether early projects can demonstrate cost control, regulatory approval and

reliable delivery timelines.

Early deployment leaders include Russia and China, which

already have SMR projects under construction or demonstration, supported by

established nuclear supply chains and state backing.

The US has a growing pipeline supported by federal funding

and regulatory reforms, but continues to face first-of-a-kind project risks.

Other markets, including the UK, Canada and several Central

and Eastern European countries, are accelerating planning but remain

constrained by costs and licensing timelines.

A major driver of demand is rising electricity consumption

from data centres, with technology companies increasingly exploring SMR

partnerships to secure stable, low-carbon power for AI and digital

infrastructure.

Despite strong momentum, challenges remain around

regulation, supply chains and public acceptance.

Analysts say

resolving these issues will be critical if SMRs are to move from demonstration

projects to a meaningful role in global electricity systems by the mid-2030s.

Attaurrahman Saibasan, Power

Analyst at GlobalData, comments: “SMR capacity is projected to increase by over

a hundredfold by 2040 relative to 2025. The substantial growth forecast is

being driven by surging demand for zero-carbon firm power, industrial cleantech

uses, and greater emphasis by policymakers on energy security.”

Saibasan adds: “Governments worldwide are implementing

supportive policies, including financial incentives, streamlined licensing

processes, and public-private partnerships, to accelerate SMR deployment. These

measures are crucial to overcome the initial financial and regulatory hurdles

associated with FOAK projects.”

Saibasan concludes: “Securing financing for FOAK SMRs requires risk sharing through public investment, guarantees, contracts for difference (CfD), regulated asset base models, or capacity payments. Investors need predictable revenue streams and clarity on regulatory and licensing commitments. Offtake agreements, utility partnerships, and industrial anchor customers can enhance bankability. Governments must consider enabling financial instruments to de-risk early projects, protect against cost overruns, and support supply chain scale-up. Early successes or failures will have outsized effects on the broader investment environment.” -OGN/TradeArabia News Service