Across the Gulf Cooperation Council (GCC), circular-economy considerations are increasingly shaping industrial planning and investment decisions.

At the same time, the region’s role as a major exporter of polymers, accounting for 4 per cent of global polymer export value in 2024, places it at the intersection of global sustainability expectations and competitive manufacturing dynamics.

As international markets place greater emphasis on product recyclability, traceability, and lifecycle performance, GCC producers face the challenge of adapting operational and data systems to meet increasingly differentiated market requirements, while continuing to leverage their established cost competitiveness.

18 per cent of GCC plastics are exported to markets with established recyclability and traceability frameworks

There are key business risks emerging from evolving global plastics frameworks and highlights areas where regional best practices can enhance resilience and market readiness without constraining growth.

STRENGTHENING MARKET READINESS

Requirements linked to product design, documentation, and traceability increasingly shape market access conditions for plastic exporters.

While producer responsibility systems differ across jurisdictions, exporters are indirectly affected through buyer expectations related to recycled content verification, mass-balance accounting, and design-for-recycling documentation.

For GCC producers, interoperability between national certification schemes and widely recognised international standards is increasingly becoming commercially relevant.

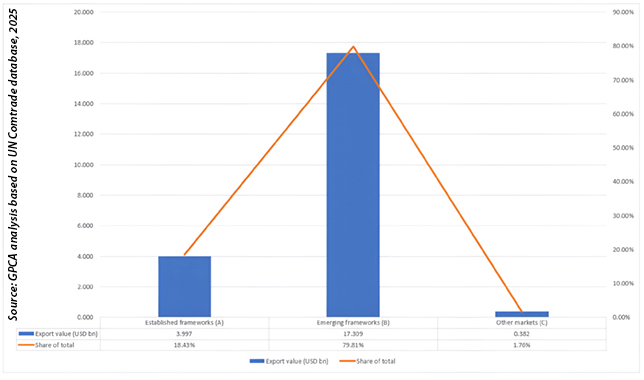

Two indicators illustrate this exposure (Figure 1):

Figure 1 ... the share of GCC plastics exports potentially subject to recyclability or traceability requirements by 2030

• Core exposure: Approximately 18 per cent of GCC plastics exports are destined for markets with established recyclability and traceability frameworks.

• Emerging exposure: Nearly 80 per cent of exports go to markets with emerging requirements by 2030.

Consequently, some export markets increasingly require recyclability documentation and traceability certificates, which could affect a very large share of exports by 2030, based on current market trajectories.

FINANCING CIRCULAR SYSTEMS SUSTAINABLY

Across many global markets, collection and recycling systems are commonly coordinated through producer responsibility organisations, funded via eco-modulated contributions or deposit-return mechanisms.

These arrangements provide dedicated funding for collection and recycling activities and generate data on material flows that can support more effective circular systems.

For exporters, the key consideration is often less the specific structure of these systems and more the transparency and predictability of associated cost signals across markets.

End-of-life system costs vary by product type. Packaging formats such as PET beverage bottles, which benefit from established collection systems and strong secondary markets, typically face lower system costs.

PE flexible films tend to incur higher costs due to more complex sorting and lower recycling yields, while PP rigid containers generally fall between these two extremes.

These costs are distributed across the value chain. Material producers may face costs related to design adaptation and certification; converters and brand owners manage compliance and reporting; and consumers may experience indirect pricing or participation signals.

As a result, the economic impact of end-of-life management is shared across stakeholders, highlighting the importance of coordination, data transparency, and product design choices in maintaining competitiveness across global plastics markets.

At the regional level, benchmarking tools that map export exposure against evolving recyclability, documentation, and traceability requirements can help companies anticipate where additional data, certification, or product adaptation may be required (Figure 2).

Figure 2 ... illustrative market readiness benchmark for GCC polymer exports (2024)

Such tools support strategic planning by translating diverse market requirements into comparable reference points.

ASSESSING THE POTENTIAL OF ADVANCED RECYCLING

Mechanical recycling remains the primary route for plastics recovery but faces limitations for mixed, multi-layer, or contaminated streams.

As a result, emerging best practices increasingly recognise advanced or chemical recycling as a complementary pathway where mechanical options are constrained or no longer viable.

In practice, the role of advanced recycling is increasingly assessed against defined performance criteria rather than technology labels alone.

These include demonstrated environmental performance on a lifecycle basis, traceability of feedstocks and outputs, controlled management of residues and by-products, and integration with existing waste-management systems.

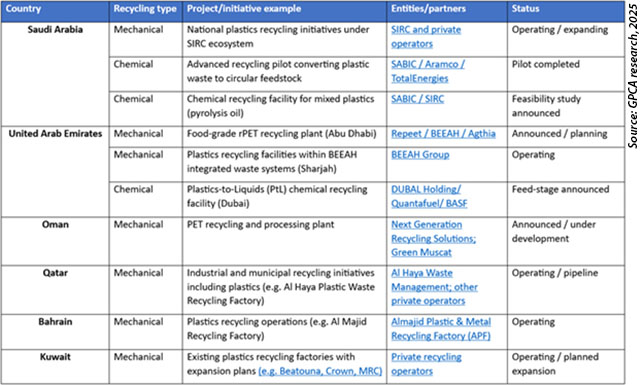

Within the GCC, chemical recycling initiatives are still at an early stage, with pilot projects and announced initiatives being explored in parallel with established mechanical recycling systems (Table 1).

From a business perspective, this creates a transitional phase in which access to certain applications or markets may increasingly depend on the availability of credible recovery pathways for complex waste streams.

Therefore, companies face strategic choices around how and when to engage with complementary recycling technologies, while ensuring that any claims are supported by robust data and verifiable performance.

MANAGING EXPOSURE IN SHORT-LIFECYCLE APPLICATIONS

Single-use and packaging applications account for a meaningful share of GCC polymer exports, primarily through the upstream supply of primary resins rather than finished products.

Changes affecting these segments do not translate mechanically into equivalent revenue losses. Instead, exposure may arise through shifts in demand composition, evolving product specifications, and pricing dynamics, particularly for upstream suppliers.

Table 1 … snapshot of announced and pilot mechanical and chemical recycling initiatives across the GCC

Mapping value streams helps identify which applications -such as films, bags, or beverage containers- are more sensitive to changes in downstream requirements.

Diversifying toward more durable applications, including construction materials, automotive components, and reusable packaging solutions, provides a natural hedge against volatility and aligns with industrial strategies focused on downstream value creation.

INTENSITY-BASED PERFORMANCE TARGETS

In global sustainability discussions, some analyses explore aggregate production limits as a potential pathway to reducing waste and emissions.

In parallel, a growing body of analysis highlights that intensity-based approaches -such as reducing emissions per ton of product, improving resource efficiency, or increasing recycled content- can deliver significant environmental gains per unit of investment.

Such approaches allow efficiency improvements to translate into measurable progress while maintaining flexibility for producers that demonstrate strong performance.

By benchmarking regional performance indicators, the GCC industry can demonstrate progress through transparent efficiency improvements rather than absolute output constraints, supporting balanced outcomes for both sustainability and economic competitiveness.

BUILDING ENABLING INFRASTRUCTURE & DATA SYSTEMS

Recycling performance ultimately depends on collection coverage, effective segregation, and reliable market outlets for recovered materials.

The Organisation for Economic Co-operation and Development (OECD) scenario modelling indicates that coordinated improvements in waste collection, sorting, and engineered disposal infrastructure could reduce plastic leakage to the environment by around 50 per cent compared with baseline pathways.

Across the GCC, high urbanisation levels have supported the development of municipal collection systems in major cities.

However, collection coverage, segregation practices, and data consistency remain uneven across jurisdictions, limiting the ability to scale recycling outcomes and capture regional efficiencies.

Beyond physical infrastructure, greater alignment of product data, material transparency, and information sharing across value chains can strengthen plastics circularity outcomes while supporting broader product stewardship objectives.

Initiatives such as harmonised waste classification codes, mutual recognition of certification schemes, and interoperable traceability frameworks can improve the flow of secondary materials across borders while safeguarding environmental integrity.

CONCLUSION

Global circularity developments do not present a single, uniform challenge for GCC polymer producers.

Instead, they translate into a set of interconnected business risks and strategic considerations shaped by market expectations, data requirements, and evolving end-of-life performance considerations across destination markets.

The GCC’s trajectory emphasises investment-led transformation, focusing on innovation, technology deployment, and voluntary alignment with global standards.

This distinction positions the region as a strategic integrator, able to blend its feedstock advantage and industrial expertise with emerging circular solutions markets.

Ultimately, competitiveness in a more circular global economy depends less on absolute production volumes and more on the ability to demonstrate efficiency, transparency, and adaptability across value chains.

By strengthening regional benchmarking, improving data interoperability, and aligning product and material information with evolving market expectations, the GCC industry can enhance resilience while preserving growth potential, positioning itself as a pragmatic and globally connected participant in the transition toward more circular plastics systems.

* The Gulf Petrochemicals and Chemicals Association (GPCA) represents the downstream hydrocarbon industry in the Arabian Gulf, and voices the common interests of more than 250 member companies from the chemical and allied industries, accounting for over 95 per cent of chemical output in the Arabian Gulf region. The industry makes up the second largest manufacturing sector in the region, producing over $108 billion worth of products a year. This article was originally published by GPCA, and can be viewed here.