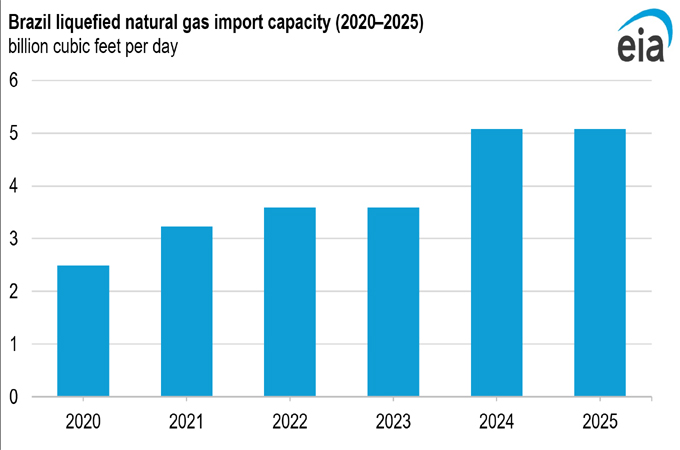

Companies operating in Brazil have expanded the country’s liquefied natural gas (LNG) regasification infrastructure since 2020, more than doubling its import capacity as the country seeks to diversify its energy supply and enhance energy security, according to US Energy Information Administration (EIA).

Brazil’s

regasification capacity grew from 2.5 billion cubic feet per day (Bcf/d) in

2020 to 5.1 Bcf/d in August 2025.

In 2024, three new

terminals added an estimated 1.74 Bcf/d of capacity: New Fortress Energy's

Barcarena Floating Storage and Regasification Unit (FSRU) with a capacity

of 0.75 Bcf/d, Terminal Gás Sul FSRU (0.50 Bcf/d), and Compass

Gás & Energia's Cosan terminal (0.50 Bcf/d).

Terminals installed

prior to 2024 include Sepetiba Bay FSRU (0.36 Bcf/d), Porto do

Açu FSRU (0.74 Bcf/d), Sergipe FSRU (0.74 Bcf/d), Bahia

FSRU (0.71 Bcf/d), and Guanabara Bay FSRU (0.80 Bcf/d).

The Suape FSRU

terminal in Pernambuco is under development and scheduled for

completion in early 2026 with an expected 0.7 Bcf/d of capacity.

Strategic drivers for LNG regasification expansion

Brazil's rapid expansion of LNG regasification capacity is driven by a

deliberate integrated LNG-to-power strategy.

Each new import

facility is paired with large natural gas-fired power plants.

For example, at the

Barcarena terminal, developers are building the 2.2 gigawatt (GW) Novo

Tempo Barcarena power station (including the CELBA 2 Power Plant,

which began early stage operations in October).

The Port of Açu

LNG terminal is associated with the 1.7 GW GNA II natural

gas-fired power plant, which began operations in May.

Regulatory mandates

have significantly accelerated Brazil’s LNG import capacity growth. In addition

to establishing the privatisation of Eletrobras, Federal Law

14,182/2021 required 8 GW of new regionalised natural gas power plant

contracting capacity.

The New Gas Law

(14,134/2021) broke Petrobras’s monopoly over natural gas production,

transportation, and distribution, opening terminals to private

developers and allowing multiple users to use a terminal to add natural

gas to the pipeline system.

Coastal LNG terminals

supply natural gas to regions lacking pipeline access and provide flexible

backup for a grid heavily reliant on renewable energy.

About 80 per cent of

Brazil’s electricity is generated from hydropower, wind, and solar.

The increased LNG

regasification capacity adds flexibility to the country’s integrated power

grid, which is particularly susceptible to droughts due to its high

dependence on hydropower.

Although hydropower

constituted 56 per cent of Brazil's electricity generation in 2024,

significant flow reductions during droughts pose a concern that hydro

generation may decrease.

Although they haven’t

significantly affected hydrogeneration, recent droughts have highlighted system

vulnerabilities, with reservoir levels in key regions falling to 29 per

cent of capacity in 2024.

Natural gas-fired plants, often linked to LNG

terminals, typically increase generation during these periods to offset

hydropower declines.

Supply dynamics

The US supplied 72 per cent of Brazil's LNG imports in 2024. Although Brazil

primarily procures LNG supplies in global spot markets due to seasonal demand

variability, it is shifting toward long-term contracts to achieve price

stability.

Notable examples

include the Centrica-Petrobras agreement with Petrobras for 0.8 million tonnes

annually over 15 years starting in 2027 and New Fortress Energy's long-term

industrial contracts with Norsk Hydro’s Alunorte refinery for

its Barcarena operations.

In addition to LNG

imports, Brazil also imports natural gas from Bolivia and

from Argentina via the GASBOL pipeline.

Brazil's domestic natural gas production reached 5.4 Bcf/d in 2024, with offshore fields accounting for 85 per cent of the output. However, 54 per cent of the natural gas produced is reinjected for reservoir pressure maintenance. -OGN/TradeArabia News Service