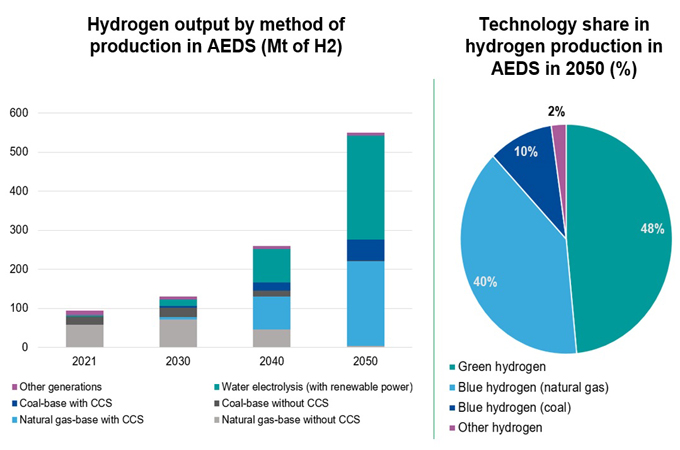

Accelerated Energy Decarbonisation Scenario (AEDS) indicate that hydrogen has the potential to play a major role in meeting future energy needs. The AEDS projects that hydrogen demand could reach 550 million tonnes (mt) by 2050, making up nearly 10 per cent of the total energy mix.

The energy sector is undergoing a transformation, with a growing focus on cleaner energy sources and technologies that reduce greenhouse gas emissions and contribute to a more sustainable future.

In this context, hydrogen is emerging as a key player in the energy transition, with a variety of clean production methods offering different advantages and competitiveness in the market.

The recent results of the Accelerated Energy Decarbonisation Scenario (AEDS), developed within the framework of the 7th edition of the GECF Global Gas Outlook, provide valuable insights into the future of hydrogen as an energy vector.

The results of the AEDS indicate that hydrogen has the potential to play a major role in meeting future energy needs. The AEDS projects that hydrogen demand could reach 550 million tonnes (mt) by 2050, making up nearly 10 per cent of the total energy mix.

This high demand for hydrogen reflects its compatibility as an energy vector, but also highlights the need for clean and more efficient means of hydrogen production.

Green hydrogen produced through the electrolysis of water using renewable power is expected to gain 48 per cent of the output by 2050, with 270 mt of production. This level of production will require a huge amount of electricity, estimated at 12,000 terawatt hour (TWh).

This is equivalent to 43 per cent of the current world annual electricity generation, or four times the current electricity generation from wind and solar, or the total current electricity generation in China and the US combined.

Moreover, there will be a massive total requirement for renewable electricity generation forecasted at 46,000 TWh annually from solar and wind in AEDS by 2050 due to higher electricity needs and decarbonisation pathways such as electrification of the energy sectors.

This massive amount of renewable power demand is more than 12 times higher than the current generation from wind and solar at around 3,600 TWh.

The need for such a large amount of renewable power makes it imperative to consider a large share of hydrogen production from other available, competitive and mature methods, such as natural gas-based blue hydrogen.

The AEDS expects that around 220 mt of hydrogen will be generated using natural gas with carbon capture and storage (CCS), accounting for 40 per cent of total output by 2050. This level of hydrogen production will require more than 930 bcm of natural gas by 2050. Coal gasification with CCS is expected to contribute to around 10 per cent or 54 mt of hydrogen production by 2050.

The cost competitiveness of these different hydrogen production methods is a key factor that will influence their market penetration and adoption. The cost of blue and green hydrogen varies depending on several factors such as location, production method, and scale of production.

Currently, blue hydrogen is a more cost-competitive option than green hydrogen, as it leverages the existing natural gas infrastructure and CCS technology.

Presently, the average cost of blue hydrogen is estimated to be around $1.5 to $3 per kilogram of hydrogen, while the cost of green hydrogen is higher, ranging from $3 to $6 per kilogram.

However, as renewable energy sources become cheaper and more widespread, green hydrogen is expected to enhance its cost-competitiveness and gain a large market share. The cost of green hydrogen production is expected to decrease by around 50 per cent by 2030, making it competitive with current cost of blue hydrogen.

On the other hand, blue hydrogen is also expected to become cheaper, as the technology for CCS improves and becomes more widely adopted. By 2050, it is estimated that the cost of green hydrogen will be similar to that of blue hydrogen, making both options viable for widespread use in various industries.

It is important to note that the energy transition is not a one-size-fits-all solution, and a variety of clean hydrogen production methods are necessary to meet the future energy needs. In this context, the AEDS acknowledges the importance of considering all clean hydrogen production methods.

Hydrogen is a crucial element in the energy transition, offering a clean and versatile energy source that can play a significant role in reducing greenhouse gas emissions and contributing to a more sustainable future.

The results of the AEDS highlight the importance of considering all clean hydrogen production methods, including blue hydrogen and green hydrogen, in the future energy mix.

The cost competitiveness of these different hydrogen production methods will be a key factor influencing their market penetration and adoption.

The energy transition will likely involve a combination of clean hydrogen production methods tailored to specific energy needs and contexts.--OGN