With the modernisation programme, Bapco’s refining capacity increased from 267,000 bpd to about 400,000 bpd

With the modernisation programme, Bapco’s refining capacity increased from 267,000 bpd to about 400,000 bpd

As the smallest GCC producer confronts depleting reserves and surging electricity demand, the Kingdom is pursuing a pragmatic hybrid strategy blending refining prowess, gas imports, and cautious renewable deployment

Bahrain stands at a critical juncture in its energy trajectory, constrained by geology yet strategically positioned to reinvent itself as a downstream and logistics powerhouse within the world’s most carbon-intensive region.

Unlike its hydrocarbon-wealthy neighbours, the Kingdom only produces 200,000 barrels of oil equivalent per day (boepd), predominantly from the ageing Bahrain Field and the offshore Abu Saafa field shared with Saudi Arabia. It also faces the Gulf Cooperation Council’s most acute depletion challenge.

Yet Bahrain’s integrated national energy champion, Bapco Energies, has emerged from a 2022 merger as one of the region’s most vertically integrated operators, combining upstream production, refining, petrochemicals, marketing, and nascent renewable ventures under a single corporate umbrella.

This consolidation reflects a broader strategic pivot: Leveraging refining scale, import infrastructure, and geographical proximity to Saudi Arabia’s Eastern Province to secure energy sufficiency even as domestic reserves dwindle.

The Kingdom’s 2030 Economic Vision and subsequent National Energy Strategy explicitly acknowledge this reality, prioritising energy security, diversification of supply sources, and incremental decarbonisation over grandiose renewable targets that lack economic foundation.

BAHRAIN’S ENERGY EVOLUTION & STRATEGIC VISION

Bahrain’s energy model has historically rested on two pillars: Modest oil production dating to 1932, and a world-class refining sector developed to process both domestic and imported Saudi crude.

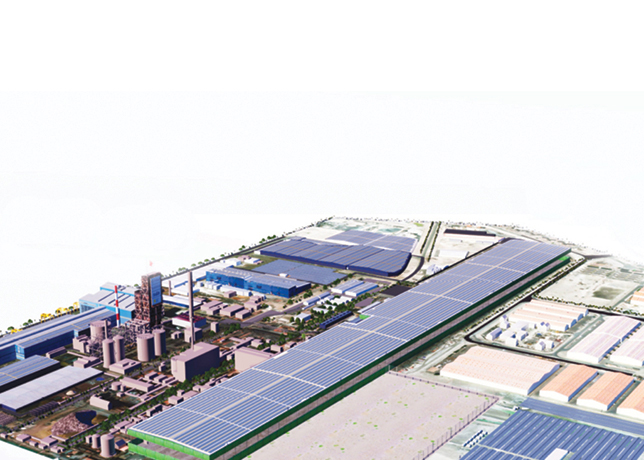

The country’s refinery, commissioned in 1936 and progressively expanded, now processes 400,000 barrels per day (bpd) following the completion of Bapco Modernisation Programme (BMP), which achieved record throughput in 2024 and represents one of the Middle East’s most significant downstream transformations of the past decade.

Shaikh Nasser bin Hamad Al Khalifa, Representative of His Majesty the King for Humanitarian Work and Youth Affairs, Chairman of Bapco Energies, announced in December 2025 that the modernised refinery had achieved unprecedented production levels one year after its formal inauguration, processing heavier crude grades and producing cleaner fuels meeting international environmental standards whilst improving energy efficiency across operations.

For decades, this configuration allowed Bahrain to punch above its weight in energy exports, but declining production from the Bahrain Field has forced a fundamental reassessment.

The government’s response has centred on three strategic pillars: Maximising recovery from existing fields, securing long-term import agreements, and gradually introducing renewable capacity to offset domestic consumption growth.

This vertical integration allows the group to optimise operations from wellhead to retail forecourt, capture margins across the value chain, and deploy capital strategically in response to market signals and national priorities.

Bahrain’s National Energy Strategy, pledges net-zero emissions by 2060, and about 20 per cent renewable penetration by 2035, a modest goal by global standards but realistic given the Kingdom’s limited land area, relatively high population density, and the absence of significant wind or geothermal resources.

The strategy also emphasises regional energy integration, particularly through gas imports from Saudi Arabia via the Abu Saafa offshore pipeline and potential future pipeline expansions, as well as liquefied natural gas (LNG) imports through the Bahrain LNG terminal commissioned in 2019.

This terminal has a capacity of 800 million cu ft per day (mmscfd), effectively doubling Bahrain’s gas supply and ensuring feedstock security for both power generation and petrochemical production.

CURRENT DEVELOPMENTS IN THE SECTOR

Bapco Energies has prioritised upstream rejuvenation through enhanced oil recovery techniques, and has focused on incremental production gains from existing fields and on downstream expansion.

During Bapco Energies’ Q4 2025 board meeting, the company reported significant achievements across its portfolio, including enhanced refinery margins, improved upstream recovery rates, and progress on renewable energy initiatives that underscore the group’s commitment to energy transition within a commercially viable framework.

On the power generation side, Bahrain’s Electricity and Water Authority (EWA) continues to procure capacity through independent power projects, with the 1,500-megawatt (MW) Al Dur 2 combined-cycle gas turbine plant, commissioned in phases from 2019, now providing the backbone of the national grid.

Renewable energy deployment has advanced cautiously, with a 150 MW solar facility underway. Expected to be completed in Q3 2027, the plant located in the southern region near Bilaj Al Jazayer, will span 1.2 sq km and will generate enough electricity to power over 6,000 homes while cutting over 100,000 tonnes of carbon emissions.

Bapco Energies has accelerated its renewable portfolio through multiple solar initiatives, including a 5-MW solar plant at its refinery that offsets a portion of the facility’s substantial electricity consumption and demonstrates the technical feasibility of integrating intermittent renewable power into energy-intensive industrial operations.

The company has also commissioned a 2.8-GW solar plant in Saudi Arabia’s Eastern Province. with Saudi developer ACWA Power.

Built over several phases, the plant will be co-located with a battery energy storage system (BESS), and power generated at the project will be transmitted to Bapco Energies.

WHERE BAHRAIN’S REAL ENERGY STRENGTHS LIE

Bahrain’s enduring competitive advantage resides not in primary hydrocarbon production but in midstream and downstream activities where infrastructure, expertise, and location converge.

The Bapco refinery complex, with its deep-water port, extensive product storage, and proximity to major Asian and European markets, functions as a critical link in regional supply chains, processing Saudi crude for export and domestic consumption.

The facility’s upgraded configuration, following the modernisation programme’s completion, enables processing of up to 400,000 bpd of heavier, higher-sulphur crude grades whilst producing ultra-low sulphur diesel, jet fuel, and other products that command premium pricing in increasingly stringent regulatory environments.

Bapco Energies’ refining margins benefit from feedstock agreements that provide crude at favourable terms, and the facility’s optimisation, incorporating hydrocracking units, delayed coking capacity, and advanced distillation, positions it competitively against regional peers whilst reducing emissions intensity per barrel processed.

The petrochemical sector, anchored by GPIC’s methanol and ammonia plants and expanding through partnerships with regional players, leverages access to competitively priced gas feedstock and established export infrastructure.

Bahrain’s aluminium smelter, Aluminium Bahrain (Alba), though not strictly part of the energy sector, represents another energy-intensive industry that has thrived due to long-term power supply agreements and operational excellence, and its expansion to nealry 1.6 million tonnes per annum (mtpa) underscores the Kingdom’s ability to sustain industrial scale despite resource constraints.

In renewable energy, Bahrain lacks the expansive desert tracts of Saudi Arabia or the UAE, but its compact geography, high solar irradiance averaging 2,200 kilowatt-hours per sq m annually, and advanced grid infrastructure provide a foundation for distributed solar and potential rooftop deployment at scale.

The Kingdom’s nascent interest in green hydrogen remains speculative but could leverage excess renewable power, desalination infrastructure, and export facilities if costs decline and demand materialises.

THE OPTIMAL PATH FORWARD

Evidence overwhelmingly supports a hybrid energy model for Bahrain, anchored by sustained hydrocarbon refining and petrochemical operations, supplemented by increasing renewable penetration to moderate domestic consumption growth and emissions intensity.

Pursuing a rapid renewable transition would undermine the Kingdom’s established industrial base, sacrifice refining revenues that underpin fiscal stability, and impose unsustainable costs on public finances already strained by subsidy obligations and infrastructure demands.

Conversely, ignoring renewable deployment would leave Bahrain vulnerable to carbon border adjustment mechanisms, reputational risks, and the long-term erosion of competitiveness as cleaner alternatives become economically compelling.

The optimal trajectory involves maximising asset life and efficiency in refining and petrochemicals, progressively integrating solar and potential wind capacity to reduce gas consumption in power generation, and exploring niche opportunities in hydrogen and carbon capture where Bahrain’s industrial ecosystem provides natural advantages.

Bapco Energies’ performance since integration validates this balanced approach, demonstrating that energy transition can proceed incrementally without sacrificing the competitive advantages that sustain Bahrain’s economy.

This approach aligns with the Kingdom’s fiscal realities, respects physical and geographical constraints, and positions Bahrain as a pragmatic energy partner within a region undergoing uneven decarbonisation.

MAJOR PUBLIC & PRIVATE PROJECTS

Bapco Energies is advancing carbon capture initiatives at its refinery, targeting initial pilot-scale projects that could eventually sequester several hundred thousand tonnes of CO2 annually, though commercial viability remains contingent on carbon pricing mechanisms and regulatory clarity.

Tatweer Petroleum, as Bapco Energies’ dedicated upstream operating company for the Bahrain Field, is implementing advanced reservoir management techniques, including water injection optimisation and horizontal drilling programmes, to arrest production decline and extend the field’s economic life.

In downstream infrastructure, Bapco Energies has commissioned new fuel storage facilities and is expanding its retail network across Bahrain and neighbouring markets, capitalising on brand recognition and supply chain integration through Bapco Trading and Bapco Retail.

GEOGRAPHICAL & LOGISTICAL LEVERAGE

Bahrain’s location adjacent to Saudi Arabia’s Dammam-Khobar industrial corridor, connected by the King Fahd Causeway and proximate to the Ras Tanura export terminal, provides unmatched access to the world’s largest crude exporter and a ready supply of feedstock and gas.

The Kingdom’s Khalifa bin Salman Port, expanded in recent years to accommodate larger vessels and increased container throughput, functions as a regional transshipment hub and could support future energy exports, including refined products, petrochemicals, or hydrogen derivatives.

Bahrain International Airport’s cargo facilities and the Kingdom’s advanced telecommunications and financial services infrastructure further enhance its viability as a logistics and trading centre for regional energy markets. The island’s compact geography allows for efficient pipeline networks, streamlined distribution, and rapid infrastructure deployment relative to larger neighbours.

Strategic initiatives such as the proposed GCC electricity grid interconnection, which would allow cross-border power trading and enhance supply security, could position Bahrain as a net importer during peak periods and a potential exporter during periods of surplus renewable generation.

Bahrain’s regulatory environment, characterised by relatively transparent licensing, established legal frameworks, and openness to international partnership, attracts investment in ways that some regional peers struggle to replicate.

DOMESTIC ENERGY DEMAND OUTLOOK

Bahrain’s electricity consumption has grown at approximately 3–5 per cent annually over the past decade, driven by population growth, industrial expansion, and rising air conditioning demand in one of the Gulf’s most humid climates.

Current peak demand exceeds 4,000 MW during summer months, with total installed capacity marginally above this level, leaving limited reserve margins and necessitating ongoing capacity additions.

Natural gas demand similarly continues to rise, fuelled by power generation, Alba’s smelter operations, petrochemical feedstock requirements, and the gradual penetration of gas in residential and commercial sectors.

Electricity and water tariffs have been reformed to reduce subsidies for households and commercial users, but industrial consumers and Bahraini nationals continue to benefit from preferential rates that blunt demand-side response.

Projections from the EWA suggest that without aggressive efficiency measures or transformative shifts in industrial structure, demand could reach 6,000 MW by 2035, requiring an additional 2,000 MW of capacity and corresponding gas supply.

Renewable penetration, even if scaled to 10 per cent of generation, would displace only a fraction of this growth, underscoring the enduring centrality of gas imports and the strategic importance of supply agreements with Saudi Arabia and LNG suppliers.

By Abdulaziz Khattak